Brookfield Corporation's Q4 2024 Results and 5-Year Outlook: A Record Year For a Steady Compounder

A global investment powerhouse with strong insider alignment and its growth trajectory

Brookfield Corporation (BN 0.00%↑) is a leading global investment business managing over $1 trillion in assets. It invests on behalf of institutions and individuals worldwide, aiming to build long-term, sustainable wealth. With a background as hands-on operators of high-quality businesses and high insiders’ ownership, Brookfield applies its operational expertise to drive growth across its portfolio and to align its leadership’s incentives to those of the shareholders. The company also co-invests alongside its partners in nearly every transaction, reinforcing a strong alignment of interests between its leadership, its customers and its shareholders.

Brookfield reported its Q4 2024 earnings and FYE 2024 results on February 13, 2025, showing strong performance across its asset management and wealth solutions businesses with accelerating growth in its cash flow: On an annualized basis, the company is generating $4.9 billion in cash flows, a year-over-year (YoY) increase of 15.3% from the prior year.

As the second largest position in my portfolio, I follow Brookfield’s strategic developments and fundamental progress. This article breaks down the key highlights from their latest earnings report and my perspective on the company’s valuation and growth outlook.

Business Segments’ Performance

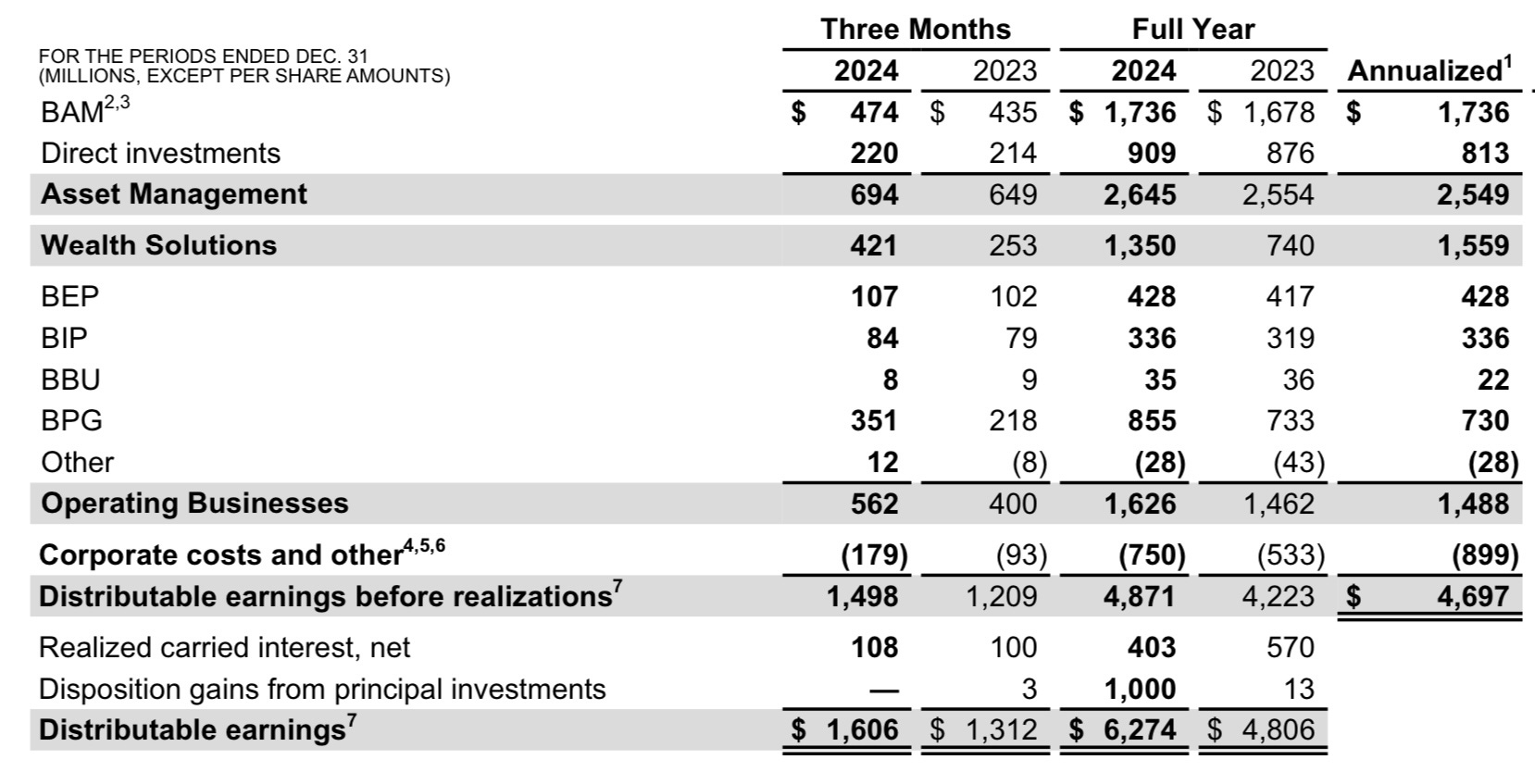

Brookfield Corporation’s Q4 2024 and 2024 year-end results highlighted solid growth across its business segments.

Asset Management

Record capital inflows: Demonstrated strength in Brookfield’s fundraising ability and investment platform expansion raising over $135 billion in new capital across various strategies.

Fee-bearing capital: Grew 18% YoY to $539 billion by year-end.

Fee-related earnings (FRE): Increased 17% YoY in Q4 and 9.6% from the prior year.

Contribution to Distributable Earnings: Generated $694 million in Q4 and $2.6 billion for the year, flat from prior year.

Wealth Solutions

Established as a top-tier annuity provider in the U.S. given a combination of successful acquisition of American Equity Life (AEL) and organic growth. Expanding operations in the U.K.

Insurance assets: Surged to $120 billion, with strong annuity sales growth. Run rate of $24 billion a year of retail capital raised.

Investment portfolio yield: 5.4%, significantly above the cost of capital.

Contribution to Distributable Earnings: Generated $421 million in Q4 (+66% YoY) and $1.4 billion for the year, up from $740 million in 2023, an increase of 82.4% from the prior year.

Operating Businesses

Brookfield Property Group (BPG), the real estate business, showed notable growth, signing 27 million square feet of office and retail leases, with rent increases of 35% over expiring leases.

When asked during the Q4 earnings call about real estate monetization given rising interest rates, Brookfield’s President, Nick Goodman explained:

“We are seeing improving liquidity and demand for high-quality real estate assets. In 2024, we monetized nearly $40 billion in assets, and we expect transaction activity to continue strengthening through 2025.”

Other segments (BEP, BIP, BBU) remained stable.

Renewable power and infrastructure: Saw 10% growth in operating Funds From Operations (FFO).

Contribution to Distributable Earnings: Generated $562 million in Q4 and $1.6 billion for the year, a modest 6.7% increase from 2023.

Distributable Earnings: Brookfield’s Profits

Distributable Earnings (DE) represent the cash flows available to Brookfield that can be distributed to shareholders or reinvested in the business. Unlike IFRS net income, which includes non-cash accounting adjustments such as fair value changes, impairments, and depreciation, DE focuses on the actual cash-generating capacity of the company’s business’ segments.

Brookfield operates as a holding company, which means IFRS financials can sometimes obscure the true economic reality of the business. IFRS earnings fluctuate significantly due to mark-to-market adjustments on investments, non-cash depreciation on long-term assets, and other accounting treatments that don’t directly impact cash flow. DE, on the other hand, provides a clearer picture of Brookfield’s underlying profitability, which is crucial for assessing its intrinsic value and long-term growth potential.

Brookfield Corporation’s financial results for Q4 and full-year 2024 reflect the company’s disciplined capital allocation and strong earnings growth across its key business segments. Brookfield continues to generate high-quality, stable cash flows while strategically reinvesting in opportunities that enhance long-term intrinsic value.

Below are key financial metrics that illustrate Brookfield’s robust performance and shareholder value creation:

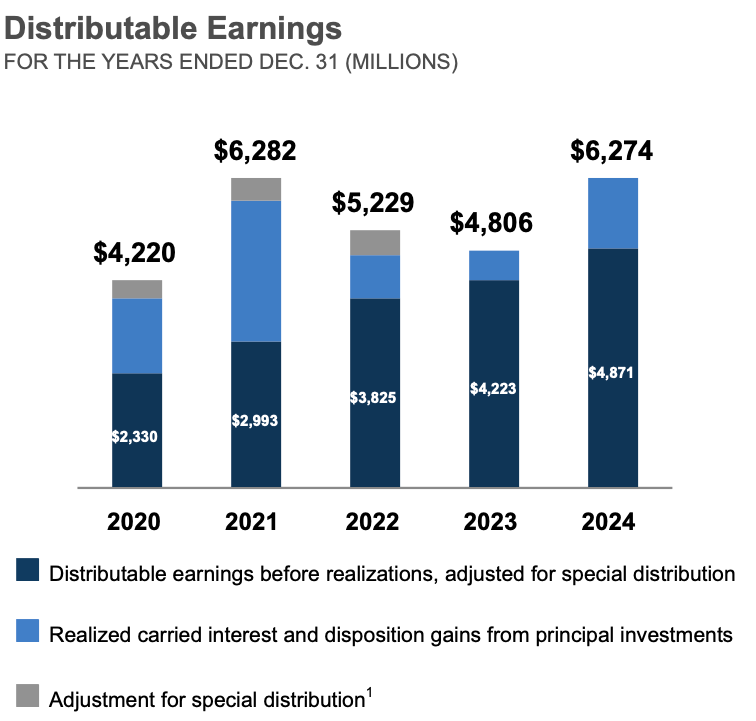

Distributable Earnings (Before Realizations):

Increased 24% YoY in Q4 and 15.3% YoY per share for the full year.

Totaled $1.5 billion for Q4 and $4.9 billion for the year ($3.1 per share).

Total Distributable Earnings (Including Realizations):

$1.6 billion in Q4.

$6.3 billion for FY 2024 ($4 per share), a 31% YoY.

$403 million in realized carried interest, from realizations in private funds managed by Brookfield Asset Management (BAM 0.00%↑) .

$1 billion in disposition gains from principal investments, primarily related to the sale of a stake in BAM to its newly acquired EAL business.

The Q4 acceleration in distributable earnings is a positive sign, aligning with Brookfield’s 5-year target of 20-25% annual growth. This exceeded my expectations and reaffirmed Brookfield’s execution capabilities.

When valuing the business I focus on distributable earnings before realizations because realizations are profits from the sale of assets, therefore it is a volatile source of earnings that, in certain years, skews profitability to the upside.

Carried Interest – A “Hidden Gem”

Brookfield’s carried interest model remains a crucial aspect of Brookfield. Carried interest is Brookfield’s share of the profits generated from its investment funds (managed by Brookfield Asset Management, a publicly-listed asset management company that Brookfield Corporation owns a 75% stake on the public market). These profits are realized when all the assets in a fund are sold and after the clients (investors in the fund) are paid. Brookfield’s share of profits is the excess above a certain minimum threshold for its clients. This strategy creates a strong alignment of interest between Brookfield Asset Management and their clients.

Unlike management fees, which provide a steady income stream, carried interest is volatile and serves as a vehicle to enhance future earnings. CEO Bruce Flatt emphasized in the Q4 shareholder letter that carried interest is a “hidden gem sitting in plain sight” and a significant future cash flow driver, stating:

“Put simply, carried interest is our share of the profits realized on an entire fund, subject to that fund exceeding a minimum target return for clients. If we meet fund expectations, we get 20% of the profits. If we earn nothing for our investors, we get nothing.”

Brookfield’s carried interest is accrued over the lifespan of a fund, but it is recognised as distributable earnings only when assets are sold and after clients are paid. Flatt highlighted:

“Much of the value creation in our investments reflected through carrying value increases or from early monetizations in a fund has yet to be recognized in our earnings. Today we have accumulated $11.5 billion of carried interest, or $7 billion net of costs, most of which we expect to recognize into our earnings over the next five years.”

When asked during the Q4 earnings call about the pace of carried interest realizations, Goodman, clarified:

“We expect a moderate increase in carried interest in 2025, but the real acceleration will likely happen in 2026 and 2027 as our funds reach later stages.”

From existing funds managed by Brookfield Asset Management, Brookfield Corporation expects to generate approximately $20 billion in cash flow from carried interest over the next decade.

Given Brookfield’s growing $240 billion in eligible Assets Under Management (AUM) and its historical track record of exceeding target returns, cash flow from carried interest has the potential to grow to $30 billion over the next ten years; a powerful long-term earnings driver that I believe is not yet reflected in the stock price.

Flatt also highlighted that Brookfield’s ability to co-invest alongside its clients and successfully execute on its investment strategy has positioned the company to continue scaling its carried interest earnings significantly in the coming years.

Balance Sheet and Capital Allocation Strategy

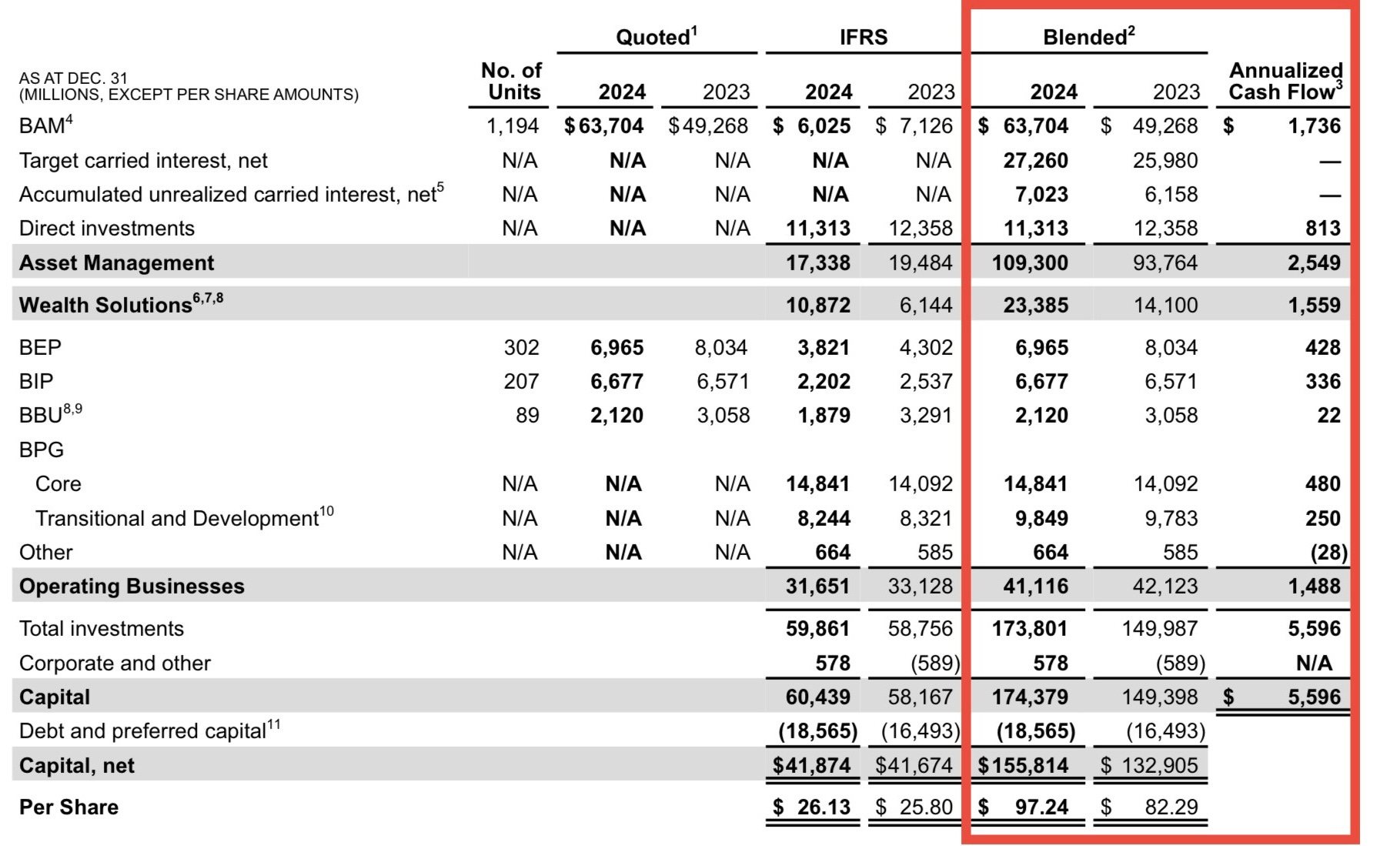

Brookfield Corporation’s capital structure highlights its substantial asset base:

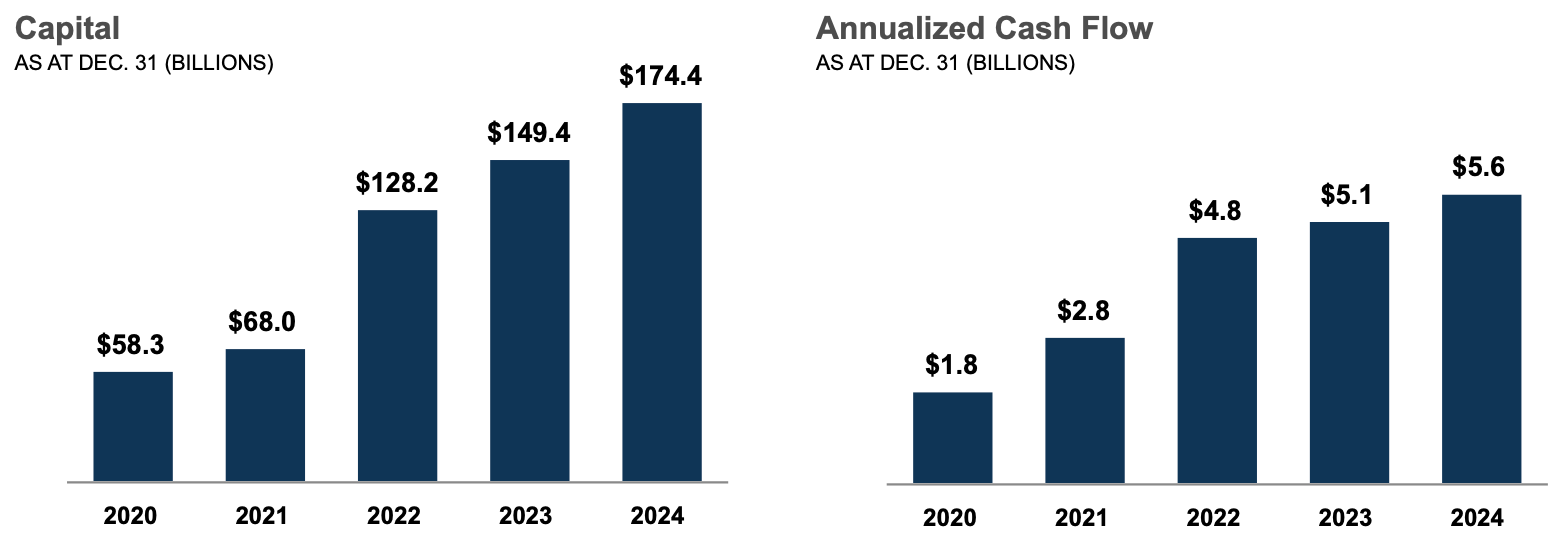

Total assets: $174.4 billion, a 16.7% YoY increase.

Debt: Long-term debt of $18.6 billion at the Corporation level averaging 14 years, and no near-term maturities in 2025.

Net Asset Value (NAV): $155.8 billion, a 17.2% YoY increase ($97.24 per share).

Annualized cash flow: $5.6 billion of diversified cash flows via dividends, which continues to grow.

Brookfield ended 2024 with $160 billion in deployable capital, positioning it well for continued investments in infrastructure, private equity and real assets.

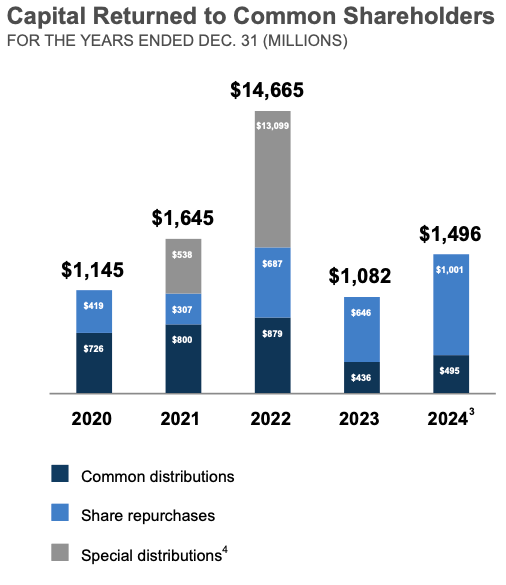

With Brookfield’s stock trading well below its calculated NAV, the company continues to buy back shares, making share repurchases highly accretive: In 2024, Brookfield repurchased $1 billion of common stock, accelerating the stock repurchase in early 2025, with another $200 million repurchased so far, increasing my stake in the company by approximately 1.5%. When asked during the Q4 earnings call about share repurchases and intrinsic value growth, Goodman responded:

“We continue to see a discount between intrinsic value and market price. This is why we repurchased over $1 billion in shares in 2024 and have already bought back $200 million in 2025.”

Having a clear preference for share buybacks, Brookfield’s returned a modest $495 million in dividends to shareholders in 2024.

In addition to return of capital to shareholders, the company deploys the majority of its cash flow towards supporting the growth of the businesses with strategic investments; a capital allocation decision that I get behind. In 2024 the majority of the distributable earnings were invested internally:

$2.4 billion into various strategies managed by BAM.

$2.3 billion investment in Wealth Solutions segment.

$1.1 billion primarily to pay down debt within the Operating Businesses.

When asked during the Q4 earnings call about Brookfield’s capital allocation strategy, particularly in Wealth Solutions (insurance) segment, Goodman responded:

“We see a combination of organic growth and bolt-on acquisitions as the best way forward in insurance. We will continue to build platforms while looking at opportunistic deals that enhance our geographic and product diversification.”

Brookfield’s Track Record of Compounding Wealth and Future Outlook

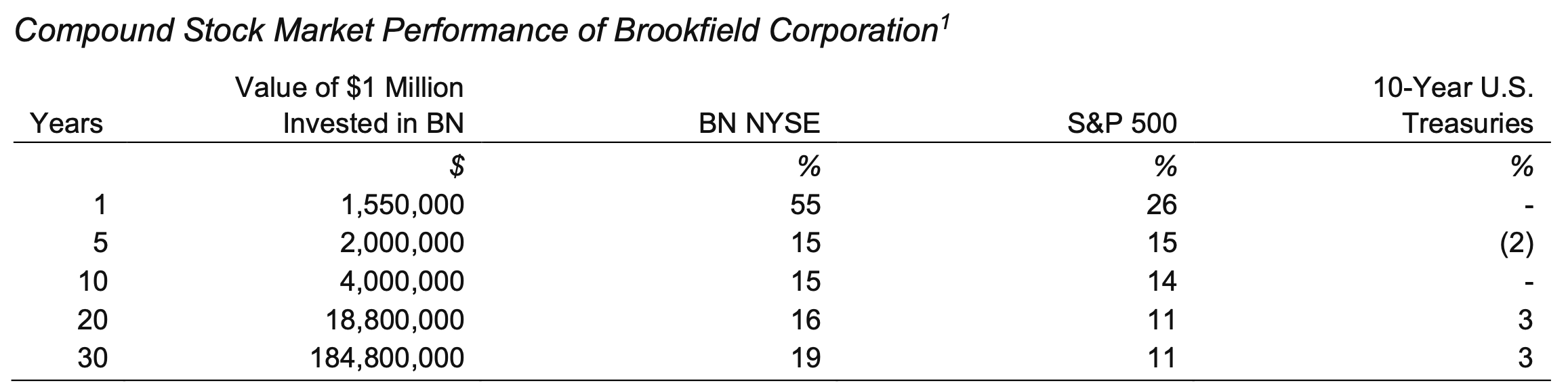

In addition to Brookfield’s policy of return of capital to shareholders, reflecting on the company’s long-term stock performance during the opening remarks of the Q4 earnings call, Flatt noted that the company’s 30-year compounded annual return is 19%, meaning that $1 million invested three decades ago would be worth $185 million today, a testament to the power of compounding.

The stock price’s surge of 55% in 2024 is a market recognition of the value creation opportunity that lays ahead: the company was deeply undervalued in late 2023. I had initiated my position in BN 0.00%↑ on October 29, 2023 at $29.02 a share and continued buying more shares in 2024. During the course of 2024, the company’s intrinsic value and its stock price have started to converge.

Brookfield has a positive outlook for 2025. The company’s leadership expects to continue its strong earnings momentum, capitalize on improving market conditions, and further compound intrinsic value through a combination of capital deployment, share repurchases, and strategic monetizations.

Valuation: Is Brookfield Corporation Undervalued?

Brookfield’s leadership, including CEO Bruce Flatt, believes that intrinsic value and cash flows will scale significantly over the next five years, reinforcing its strategy of compounding capital efficiently. According to Flatt, “intrinsic value in 2024 increased by 19%” to $97.24 per share. The current stock price of $60.92 is selling at a 37.4% discount to intrinsic value. On shareholder value, Flatt reaffirmed Brookfield’s commitment to increasing intrinsic value.

Brookfield’s current market capitalization fluctuates around $92 billion. The Price to Distributable Earnings Before Realizations (Brookfield’s equivalent of the P/FCF) sits at 18.7x while peers like Apollo Global Management and KKR trade above 22x P/FCF.

The company is on track to grow distributable earnings 20% annually over the next five years, with potential to recognize an additional $7 billion of net accumulated carried interest into earnings within five years, further enhancing cash flows.

Brookfield also intends to continue buying back shares when trading below their intrinsic value. This return of capital policy would amplify distributable earnings per share and increase shareholders’ stakes in the company.

A Discounted Cash Flow (DCF) model using the low-end 20% of the company’s guided 20-25% growth rate of distributable earnings, attaching a realistic 20x P/DE multiple, assuming the company will buy back 1% of its outstanding common shares each year, and using a conservative 10% discount rate, suggests a fair value of $97.83 per share today which is around what Flatt believes the current intrinsic value of the business is. With these assumptions, on today’s price, the stock offers a 21% CAGR upside potential over the next five years, meaning the stock is trading at a discount to intrinsic value despite Brookfield’s strong cash flow growth and carried interest potential.

This valuation disconnect is why Brookfield continues to repurchase shares despite the stock price’s surge of 55% in 2024.

Final Thoughts

Brookfield Corporation’s Q4 and full-year 2024 results reinforce my bullish stance on the company. With its diversified business model, consistent earnings growth, strategic share buybacks, and substantial carried interest potential, Brookfield remains an attractive long-term investment.

Under its experienced leadership, Brookfield is well-positioned to continue executing its growth strategy, compounding organic distributable earnings growth and monetizing carrier interest. I expect the market to increasingly reflect its intrinsic value positioning its stock to deliver substantial market-beating returns.

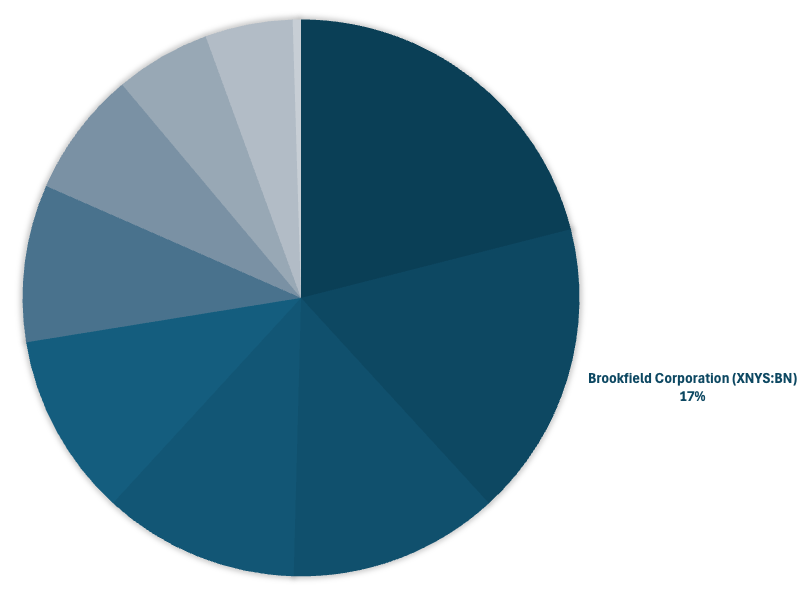

Given its strong fundamentals and a projected 20% annual growth rate, Brookfield remains my second-largest holding, currently comprising 17% of my portfolio.