The Cost of Hesitation: Lessons From Errors of Omission, Sunk Cost Fallacy, and Opportunity Cost

Reflections on mistakes that shaped my investment philosophy

“There’s no way that you can live an adequate life without making many mistakes. In fact, one trick in life is to get so you can handle mistakes. Failure to handle psychological denial is a common way for people to go broke. You can’t learn if you can’t admit reality. It’s that simple.”

— Charlie Munger

Mistakes are an inevitable part of life, and investing is no exception. As Charlie Munger so aptly puts it, the real challenge isn’t avoiding mistakes, it’s learning how to face them, understand them, and grow from them.

In this spirit, I’ve come to view my own investing journey as a continuous cycle of trial, error, and reflection. Each mistake is a chance to refine my approach, strengthen my discipline, and ultimately become a better investor. In this article, I’ll share how hesitation and emotional attachment led to investing mistakes and the lessons I learned to avoid repeating them.

By reflecting openly on these errors, I hope to not only hold myself accountable but also offer insights to level-headed investors navigating similar challenges. After all, as Munger reminds us, learning from mistakes, our own and those of others, is one of the most powerful tools in the investor’s arsenal.

Errors of Omission: The Missed Opportunity in Netflix in 2022

Errors of omission occur when an investor fails to act on a well-researched opportunity, often due to hesitation, fear, or an overemphasis on short-term challenges. Unlike errors of commission, where the decision to invest leads to a loss, errors of omission represent the missed potential of untapped opportunities. One notable example from my investing journey was my hesitation to invest in Netflix (NFLX 0.00%↑) in 2022.

In that year, Netflix faced significant market pessimism as it reported its first-ever consecutive quarterly net subscriber losses, fueling fears of market saturation and rising competition. Macroeconomic pressures further eroded investor confidence, causing the stock to nosedive amid concerns that Netflix’s growth story was over. Despite its reputation as a streaming leader, bearish sentiment overshadowed the company’s adaptability and economies of scale, creating a perfect storm for its stock price:

Subscriber declines: Netflix reported its first-ever net losses in total subscribers, 200,000 in Q1 and nearly 1 million in Q2, with the Q2 loss largely driven by the company’s decision to exit Russia, which accounted for approximately 700,000 subscribers. This led to a 35% stock drop after the Q1 earnings report.

Rising competition: Disney+, and others aggressively gained ground, challenging Netflix’s dominance.

Macroeconomic pressures: Inflation and recession fears reduced household spending on discretionary services like streaming.

Business model issues: Over 100 million households shared Netflix accounts’ passwords, limiting revenue, while plans for ad-supported tiers and monetization changes were seen as reactive.

Bill Ackman’s Bet on Netflix and His Exit

In January 2022, Bill Ackman’s Pershing Square Capital Management invested $1.1 billion in Netflix, acquiring over 3.1 million shares. With a press release on January 26, 2022 Ackman expressed confidence in the company’s leadership and growth potential. However, by mid-April 2022, Ackman liquidated the position after Netflix’s Q1 earnings report.

In his letter to fund holders on April 20, 2022, Ackman explained that subscriber losses and new initiatives like advertising and password sharing reforms added significant uncertainty to Netflix’s business model. He noted:

“While we believe these business model changes are sensible, it is extremely difficult to predict their impact on the company’s long-term subscriber growth, future revenues, operating margins, and capital intensity.”

Ackman emphasized that Netflix no longer met Pershing Square’s requirement for predictability, leading to a ~$400 million loss and a 4% reduction in the Pershing Square’s year-to-date performance.

Why I Disagreed with Ackman and the Market

Despite the challenges Netflix faced in 2022, I believed the bearish sentiment was overblown, and Ackman’s decision to sell was premature. Here’s why:

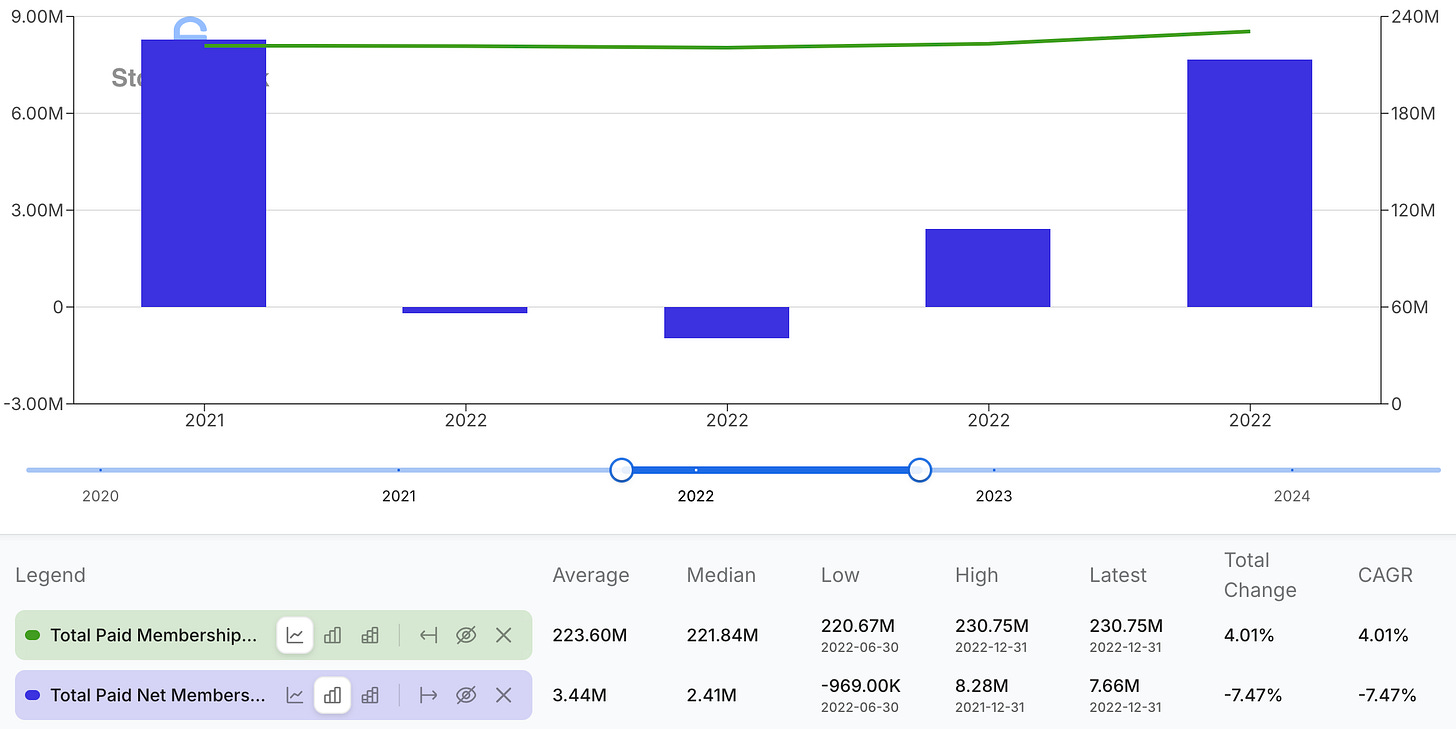

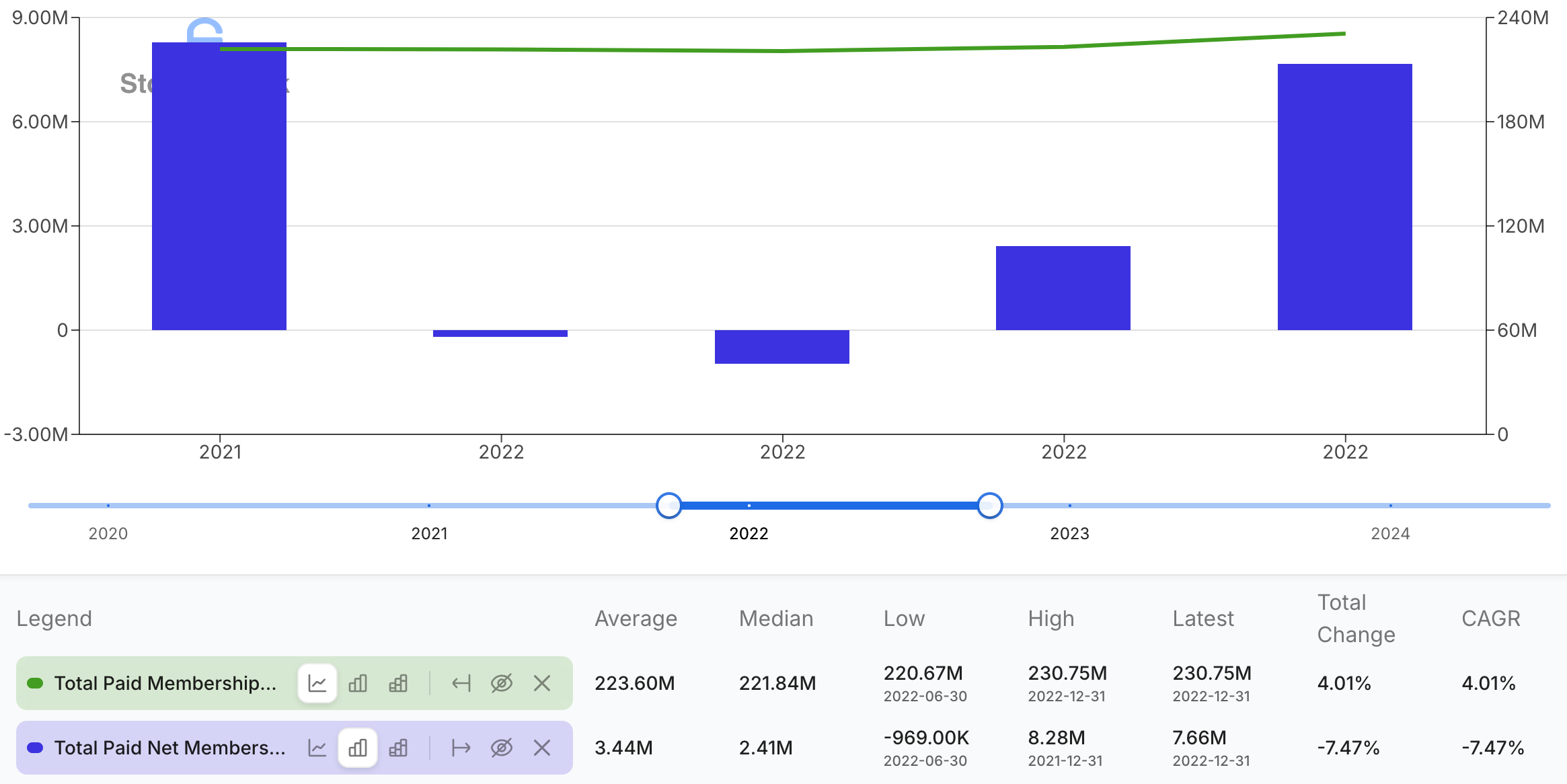

Short-term noise vs. long-term fundamentals: The subscriber declines in Q1 and Q2 were not indicative of a structural decline. They were largely a reaction to macroeconomic headwinds and post-pandemic normalization. In the next quarter, Q3 2022, Netflix had gained 2.4 million net subscribers and ever since, it has recovered its subscriber growth trajectory, proving its resilience.

Netflix total paid subscribers (green line) and its total net subscriber change quarter-over-quarter (blue bars) - the graph shows a net loss in subscribers in Q1 and Q2 2022 only to accelerate growth ever since Q3 2022 Adaptability: Netflix’s decision to introduce an ad-supported tier and crack down on password sharing were seen by market commentators as reactive moves. I viewed them as necessary and calculated adaptations to changing market dynamics. By 2024, both initiatives were key drivers of improved free cash flow and profitability.

Ad-supported tier: Launched in late 2022, it quickly attracted cost-conscious subscribers and advertisers, boosting Average Revenue Per User (ARPU) and driving incremental revenue growth by 2023.

Password sharing crackdown: Gradually implemented, it converted shared accounts into standalone subscriptions, significantly increasing the subscriber base and revenue.

Strong content and global reach: Netflix continued to invest in high-quality, globally appealing content. Hits like season 4 of Stranger Things, Wednesday, Dahmer, and international blockbusters underscored its ability to attract and retain viewers. Its global reach remained unmatched, widening its competitive edge also in emerging markets.

The subscriber losses turned out to be temporary. By late 2022, Netflix had not only recovered but also diversified its subscription offerings with ad-supported tiers and strengthened its content pipeline.

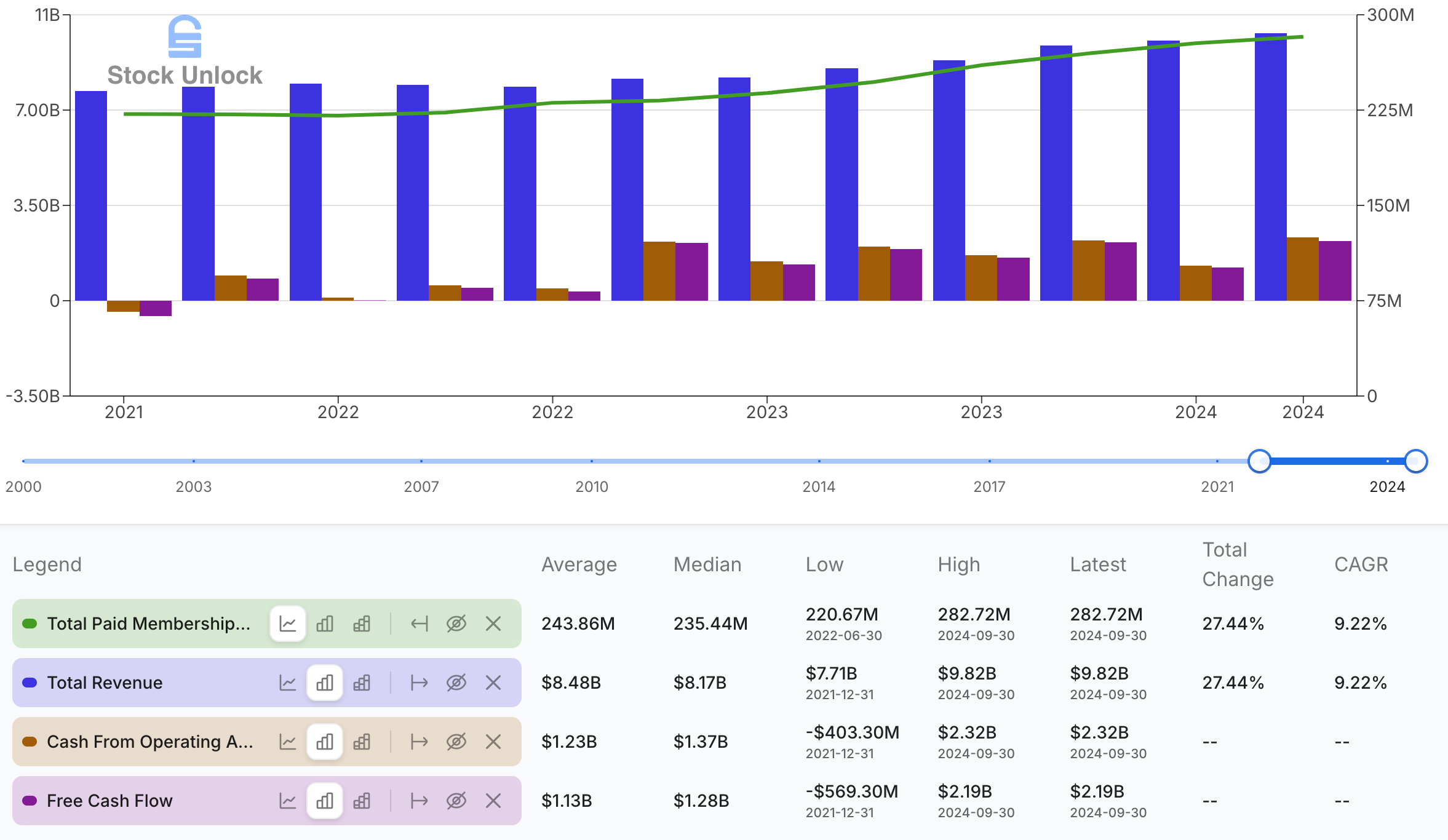

Fast forward to late 2024, Netflix had solidified its comeback. Paid subscribers reached a record 282.72 million, revenue grew steadily from $7.87 billion in Q1 2022 to $9.82 billion, and free cash flow surged to $2.19 billion, a dramatic turnaround from its negative position in Q4 2021. These results reflect Netflix’s operating leverage, ability to adapt, and build a more sustainable, profitable business model. Since its lows in mid-2022, Netflix’s stock has risen over 400%, underscoring the market’s recognition of its resilience and renewed growth potential.

Despite having researched and built conviction in Netflix for some time, I didn’t act, a classic example of action inertia, where hesitation and fear of making a mistake prevent decisive action. I allowed prevailing market sentiment to overshadow the long-term fundamentals of the business, ultimately missing a clear opportunity to invest in a prime asset at a discounted price. In hindsight, Netflix was well-positioned to overcome its challenges.

The Sunk Cost Fallacy: Holding on to Scottish Mortgage Investment Trust

On the flip side of errors of omission lies the sunk cost fallacy, the psychological trap where investors hold onto an investment longer than they should, driven by emotional attachment or a reluctance to acknowledge a mistake. Rather than focusing on the future potential of an investment, decisions are clouded by the time, money, or effort already committed, which are irrecoverable. This bias not only results in holding onto under-performing investments but also incurs a significant opportunity cost: the cost of missing out on reallocating capital to higher-conviction opportunities.

This dynamic became evident in my handling of Scottish Mortgage Investment Trust (SMT), where my hesitation to sell delayed my ability to invest in better-aligned opportunities. I invested in SMT in early 2021, drawn to its focus on disruptive innovators like Tesla (TSLA 0.00%↑) and Moderna (MRNA 0.00%↑). The narrative of backing the “next big thing” was captivating, even as rising interest rates exposed vulnerabilities in its high-growth, cash-burning portfolio. SMT’s approach conflicted with my valuation-driven principles. Its reliance on lofty projections felt increasingly speculative, yet I hesitated to act, unwilling to confront the reality of this misalignment.

By the time I sold SMT in late 2024, the decision was overdue. The emotional attachment to its narrative had prevented me from reallocating capital earlier to businesses like Alphabet (GOOGL 0.00%↑) and Brookfield Corporation (BN 0.00%↑) , which better aligned with my process. This delay incurred a significant opportunity cost.

Lessons Learned

Reflecting on my experiences with Netflix and SMT, several key lessons stand out. These insights not only serve as reminders for my future decision-making but may also resonate with fellow investors navigating similar challenges:

Act on conviction: Building conviction through research is only half the battle; the other half is having the courage to act on it. Despite understanding Netflix’s underlying strengths, I allowed fear and uncertainty to prevent me from capitalizing on a clear investment opportunity.

Separate short-term noise from long-term value: Netflix’s 2022 subscriber losses and market pessimism were short-lived challenges, not structural declines. My hesitation to invest highlights the importance of focusing on a company’s fundamentals, resilience, and long-term potential rather than being swayed by temporary setbacks or market sentiment.

Stay aligned with my principles: The misalignment between SMT’s moonshot bets strategy and my analytical, valuation-focused approach led to a delayed decision to sell, driven more by the allure of its past narrative than genuine conviction in its future potential. Ensuring that every investment aligns with my process and philosophy is vital to maintaining discipline and avoiding regret. I’ve since rectified this mistake in 2024 by realigning my portfolio with my principles, a process I’ve explored further in a separate article.

Avoid emotional attachment: The sunk cost fallacy with SMT underscored the dangers of emotional attachment to an investment. Decisions should be forward-looking, based on alignment with my investment philosophy and the potential for future growth, not on past commitments or narratives.

As Charlie Munger wisely said, the real challenge isn’t avoiding mistakes but learning from them. Both errors of omission and the sunk cost fallacy provided valuable lessons that have refined my approach and reinforced the importance of disciplined, long-term thinking.

Final Thoughts

Reflecting on these experiences has been humbling. Mistakes are inevitable in investing, and their true value lies in the lessons they impart. Acknowledging and learning from these missteps allows me to refine my approach, strengthen my discipline, and make more informed and confident decisions in the future.

“A man who has committed a mistake and doesn’t correct it, is committing another mistake.”

— Confucius

Whether it’s failing to act on conviction or holding onto an investment for the wrong reasons, each error underscores the importance of disciplined, forward-looking decision-making. For level-headed investors, these reflections serve as a reminder that mistakes are not signs of failure but opportunities for growth.

What about your own investing journey? Have you ever hesitated to act on conviction or held onto an investment longer than you should have? How did those decisions affect your portfolio, and what changes did they inspire in your approach? Reflecting on these questions can be a powerful exercise in self-awareness, helping you align your decisions with your principles and long-term goals.

Remember, every mistake, whether an error of omission or a sunk cost fallacy, is a step toward becoming a wiser, more disciplined investor. The key is not to avoid mistakes entirely, but to ensure that each one leaves you better prepared for the next opportunity.