Volatility Isn't Risk: Lessons in Temperament and Conviction

How to view market swings as opportunities, not threats

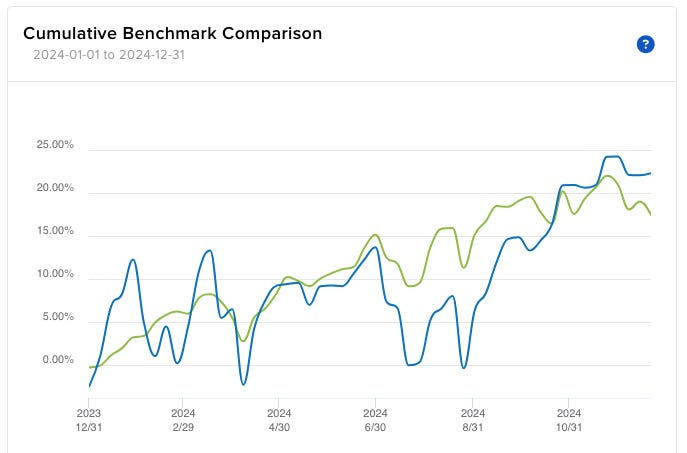

In investing, numbers often reflect a broader narrative. The blue line in my portfolio’s 2024 performance chart illustrates a journey of conviction and the ability to navigate volatility with discipline. Over the span of 12 months, my concentrated portfolio experienced sharp fluctuations, with gains evaporating entirely in mid-April, early August, and again in early September, before recovering strongly later in the year. Despite these challenges, I stayed the course and avoided panic selling. This approach was not accidental but deliberate. As Warren Buffett famously said:

“The most important quality for an investor is temperament, not intellect. You need a temperament that neither derives great pleasure from being with the crowd or against the crowd.”

In moments like August 2024, when my theoretical gains were wiped out within days, it was temperament, not market foresight or complex models, that dictated my actions. I trusted my research and my conviction in the businesses I own. Without conviction, fear and emotions can easily take over. This discipline is rooted in a principle championed by Peter Lynch:

“Know what you own, and know why you own it.”

Reframing Volatility: A Path to Opportunity

Is volatility truly the same as risk? Traditional financial theory says yes, but seasoned investors know better.

In traditional financial theory, particularly Modern Portfolio Theory (MPT), volatility is equated with risk, with metrics like the Sharpe ratio1 using it as a proxy. However, I align with legendary investors such as Warren Buffett, Dev Kantesaria, managing partner and portfolio manager at Valley Forge Capital, and Seth Klarman, CEO and portfolio manager at Baupost Group who argue that volatility does not equal risk.

“In business schools, volatility is almost universally used as a proxy for risk. Though this pedagogic assumption makes for easy teaching, it is dead wrong: Volatility is far from synonymous with risk. Popular formulas that equate the two terms lead students, investors and CEO’s astray.” — Warren Buffett

“The business school model is you have to use the volatility of the stock as a major input as risk. Now volatility is not always a great measure of risk on a going-forward basis.” — Dev Kantesaria

“We steer clear of the foolhardy academic definition of risk and volatility, recognizing, instead, that volatility is a welcome creator of opportunity.” — Seth Klarman

As Klarman notes, the very volatility that academic models fear can create the most compelling opportunities for disciplined investors.

Unpacking the Psychology Behind Market Swings

While academic models focus on volatility, behavioral finance reveals a deeper truth: market swings are often driven by collective human psychology rather than fundamental changes. Research by Daniel Kahneman and Amos Tversky in 1979 on loss aversion highlights how emotional reactions to perceived losses amplify volatility. Their Prospect Theory demonstrates that people experience the pain of losses more intensely than the pleasure of equivalent gains, leading to irrational decision-making under uncertainty. This tendency often causes investors to overreact to negative news, triggering selloffs and intensifying market swings.

For example, when markets decline, investors disproportionately focus on minimizing further losses rather than evaluating the long-term intrinsic value of their holdings. This behavior often cascades into herd-like selling, further disconnecting stock prices from underlying fundamentals. A recent study published in the Behavioural Public Policy journal similarly highlights how biases like herd mentality and overconfidence contribute to volatility, exposing the psychological roots of market fluctuations.

Benjamin Graham’s allegory of Mr. Market underscores this idea, portraying the market as a highly emotional character who alternates between irrational optimism and pessimism. As Graham observed:

“The investor’s chief problem - and even his worst enemy - is likely to be himself.”

I explored Graham’s timeless wisdom from The Intelligent Investor in a previous post, delving into his emphasis on avoiding emotional decision-making.

By understanding that volatility is frequently psychological rather than fundamental, level-headed investors can navigate market fluctuations more effectively and assess risk with greater clarity.

Decoupling Volatility from Risk: Turning Market Swings into Opportunity

While I don’t claim to have superior insight compared to other investors and operate with the same publicly available information, I view volatility as an inherent and unavoidable aspect of investing, especially as long as I remain a net buyer of stocks: When stock prices fall sharply, I see them as opportunities to acquire productive assets I believe in at more attractive prices, provided the underlying fundamentals remain sound.

Dev Kantesaria, a proponent of viewing volatility as opportunity, echoed similar sentiments in a 2022 interview:

“We view our advantage first in the form of temperament. We don’t get happy when the market goes up, we don’t get sad when it goes down. We’re not about what we’re going to make this quarter, this year, or even next year.”

Kantesaria’s philosophy resonates deeply with my own approach. Like him, I view short-term fluctuations as irrelevant distractions when the long-term investment thesis remains intact. Rather than seeing volatility as a signal to sell, I embrace it as an opportunity to optimize my portfolio by doubling down on high-quality assets at more attractive prices. The sharp drops in my portfolio value in 2024 were opportunities to act decisively and reinforce my positions: In August 2024, I made the decision to liquidate a position in a holding which I had begun building just a few months earlier. The sale, executed at a marginal gain, was driven by an opportunity during the market selloff, allowing me to redeploy the proceeds into my high-conviction holdings, in line with my belief in concentrating capital where I see the greatest long-term potential.

Volatility and Market Reactions: When Good News Becomes Bad News

Volatility often arises from how markets participants react to shifting expectations. For example, on January 10, 2025 the U.S. posted stronger-than-expected employment numbers, with unemployment falling to 4.1%. Despite signaling a strong economy, the S&P 500 dropped 1.54% on the day.

Why? A robust economy makes it less likely that the Federal Reserve will lower interest rates, disappointing investors who anticipated rate cuts. Higher rates mean higher borrowing costs and potentially lower valuations (a dynamic I’ve covered in a previous article), prompting a selloff.

This counterintuitive reaction highlights a key aspect of volatility: it’s often about shifting expectations, not fundamentals. For level-headed investors, such moments are reminders to focus on underlying business quality and view price declines as opportunities to buy at more attractive prices rather than risks. As Li Lu, founder and chairman of Himalaya Capital and close friend of the late Charlie Munger, echoes this sentiment:

“Not only is the mere drop in stock prices not risk, but it is an opportunity. Where else do you look for cheap stocks?”

Staying the Course: How Conviction Triumphs Over Fear

Concentrated portfolios can amplify volatility, but they also amplify returns, provided the underlying businesses remain strong. The steep drops I endured in 2024 were not failures but tests of conviction, reaffirming my belief that temperament matters far more than timing. I didn’t lose sight of the intrinsic quality of my holdings, even when the market briefly did. As Peter Lynch aptly noted:

“The real key to making money in stocks is not to get scared out of them.”

Had I panicked during the selloffs in 2024, the subsequent rebound in my portfolio would never have occurred. At their lowest points, some positions were down significantly, and selling out of fear would have meant missing the recovery and locking in losses. Instead, by weathering the storm, I positioned myself to benefit as the market rediscovered the value of the high-quality assets I own.

Final Thoughts

The sharp fluctuations in my portfolio’s performance during 2024 were not anomalies but rather reflections of the natural rhythm of stock markets, especially for a concentrated portfolio. These swings reaffirm a core truth about investing: the ability to endure volatility with discipline and act rationally in uncertain times matters more than any theory or model.

Investing is a long-term endeavor, and its rewards lie in the willingness to weather temporary discomfort for lasting gains, as Charlie Munger aptly noted:

“The big money is not in the buying and the selling, but in the waiting.”

Legendary investors like Warren Buffett, Peter Lynch, and Seth Klarman have consistently emphasized that temperament and a deep understanding of one’s holdings are the cornerstones of successful investing. Volatility, while inevitable, is not an adversary but a powerful ally for level-headed investors with the patience and conviction to recognize its opportunities. As Buffett wrote in Berkshire Hathaway’s 1986 shareholder letter:

“We simply attempt to be fearful when others are greedy and to be greedy only when others are fearful.”

This philosophy forms the foundation of my investment approach. By staying the course and focusing on the long-term value of quality businesses, I strive to turn market turbulence into a tool for compounding returns.

The Sharpe ratio is a measure of risk-adjusted return that evaluates how much excess return an investment generates per unit of risk, calculated as the difference between the investment’s return and the risk-free rate (such as the yield of the 10-year U.S. treasury note), divided by the investment’s standard deviation.